What to Expect from the Capital Markets in 2026

The past year was everything but dull. Geopolitical tensions, surprising market movements, and especially rapid technological advancements have shaped the capital markets. One topic stood out in particular: Artificial Intelligence (AI).

But what does this mean for investors in the year 2026? Which trends will persist, where will new risks emerge, and where will opportunities arise beyond the well-known tech giants?

Where is the growth happening? In the infrastructure of the AI-Boom

The capital markets of recent years have been strongly dominated by a single major trend: Artificial Intelligence. What initially began as an evolutionary advancement in the semiconductor industry has developed into an unprecedented concentration of market power.

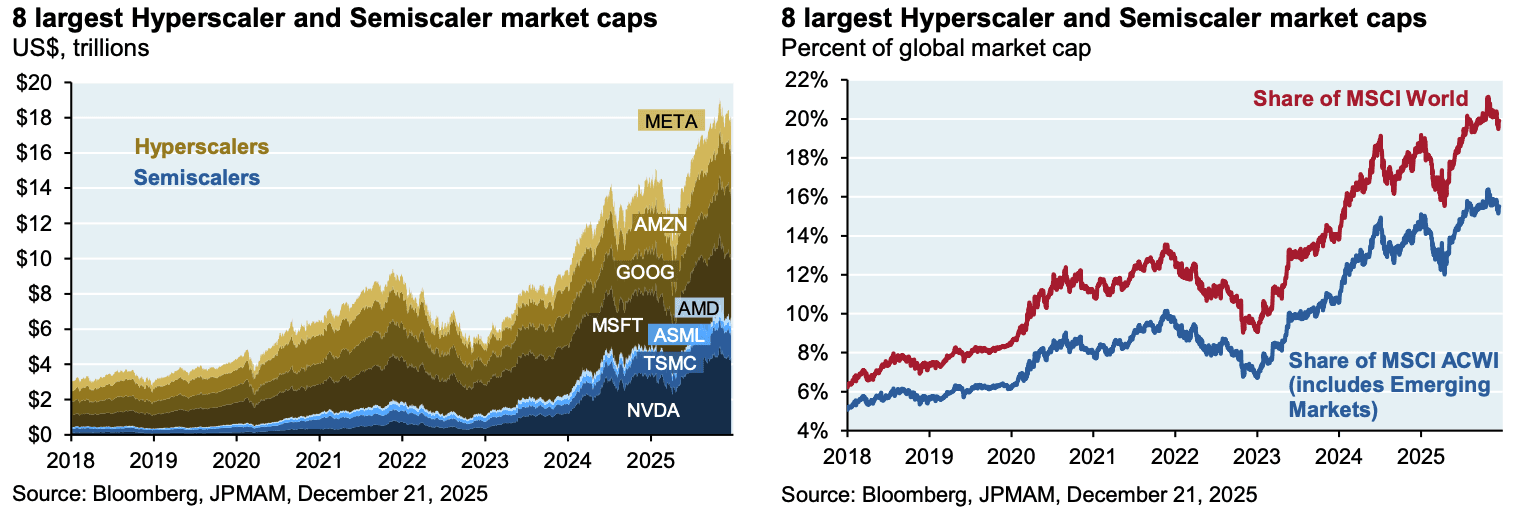

Companies like NVIDIA, TSMC, and ASML are no longer merely suppliers. They form the technological foundation of the entire AI value chain — from chip design and manufacturing to highly specialized lithography. Together with the major US hyperscalers (Microsoft, Amazon, Alphabet, Meta), they have built a structural competitive advantage that is hardly vulnerable in the short term.

Since the launch of ChatGPT in 2022, around 42 directly AI-related companies accounted for between 65% and 75% of the total profit growth, revenue dynamics, and investments of the S&P 500. The market capitalization of the four hyperscalers plus the three leading semiconductor companies increased from around $3 trillion to about $18 trillion in just a few years. The following graphics illustrate this development:

USA vs. Europe: Why the market appears so unbalanced

This concentration is also reflected at the macroeconomic level: In recent quarters, approximately 40–45% of the total US GDP growth was attributable to the technology sector.

This is particularly relevant for European investors. Without the strong performance of US AI stocks, the S&P 500 would have significantly underperformed compared to Europe, Japan, and China. The relative lead of the USA is thus almost entirely based on the AI sector — while large parts of the broader market have hardly benefited from it.

Energy and Capital: The critical factors of the AI era

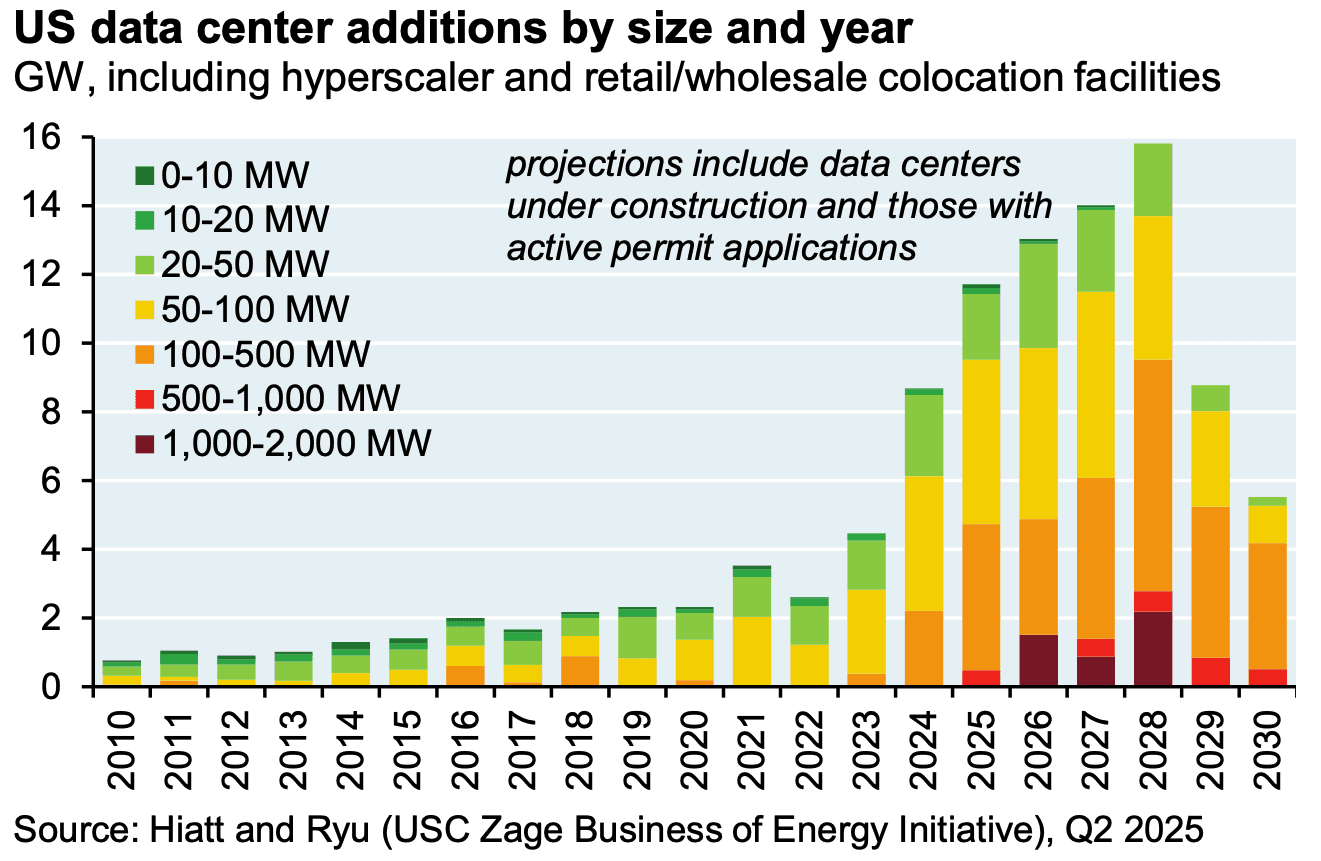

The technological lead of major AI companies is real. At the same time, new structural dependencies are emerging. Two factors are coming into focus: Energy supply and financing models.

Global electricity demand is rising significantly — driven by digitalization, data centers, and AI infrastructure. At the same time, many economies are in the midst of transforming their energy systems. Energy thus becomes a strategic production factor again.

For 2026, this means:

increased investment needs in grids, storage, and generation

greater importance of supply security

growing differences between regions and companies

Companies with stable access to affordable energy secure clear competitive advantages. For investors, there are opportunities along the entire energy value chain — from infrastructure through utilities to specialized suppliers.

AI scales — and so does the capital requirement

For a long time, the major technology companies financed their investments almost entirely from operating cash flow. The leading AI players, in particular, were considered debt-light and extremely capital-strong. But with the rapid expansion of data centers and AI infrastructure, this picture is changing.

The reason is simple: The investment volumes are now reaching a magnitude where even very high ongoing cash flows are no longer sufficient to flexibly finance growth. Therefore, a part of the financing is increasingly shifting to the debt markets.

Two examples illustrate this trend:

Oracle is increasingly financing the expansion of its cloud infrastructure for OpenAI through external capital.

Meta has created a special purpose vehicle (SPV) with Blue Owl for its Hyperion data center in Louisiana. Through this vehicle, around $27 billion of investment-grade debt was raised.

These financing models decouple large projects from the operational business and partially shift risks to capital markets. Even if the balance sheet impact is limited, a clear trend is emerging: AI expansion is no longer solely financed through cash flows. This makes interest rates, refinancing costs, and capital market access relevant risk factors for tech giants.

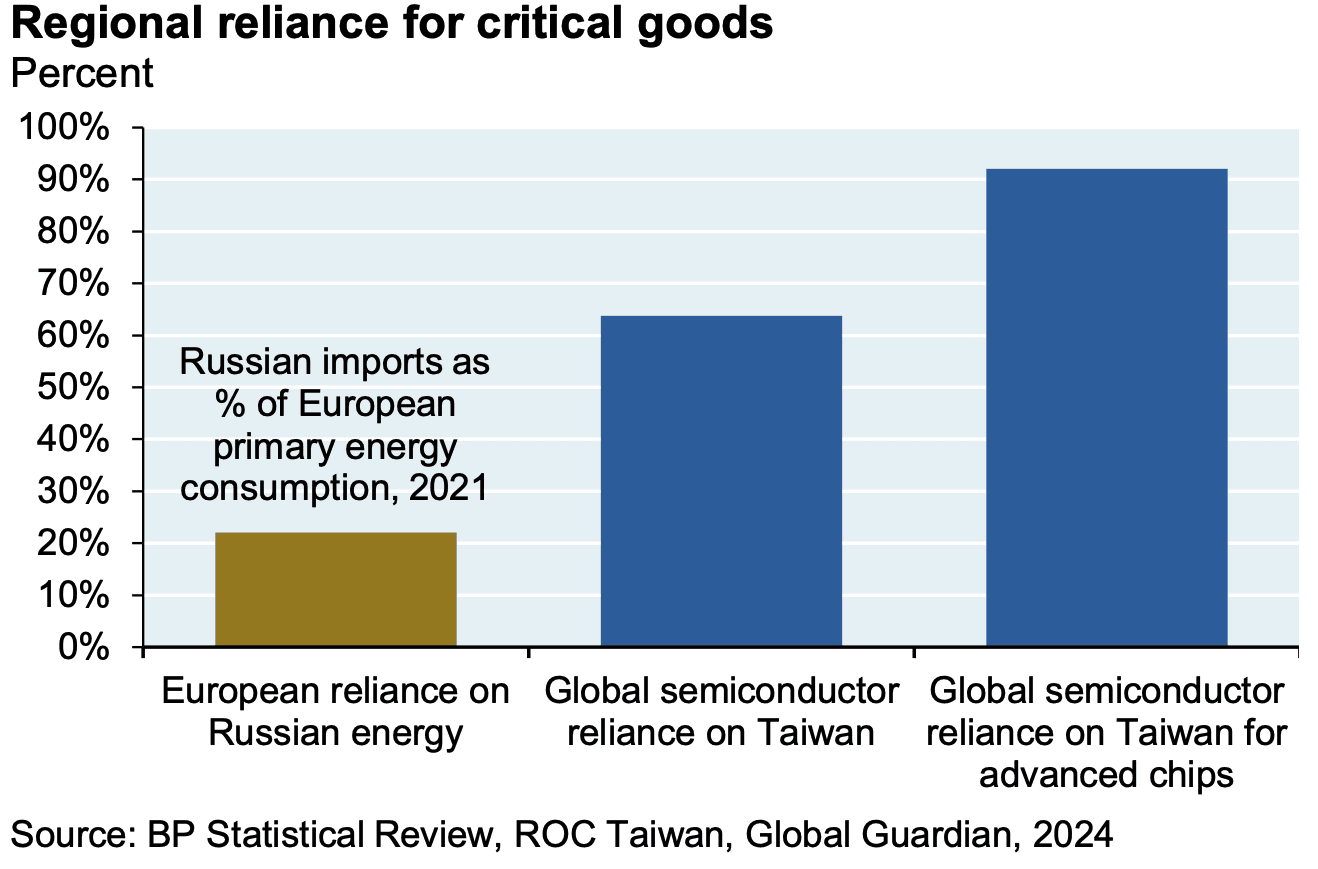

Semiconductor dependence as a systemic market risk

The Achilles' heel of the AI value chain is Taiwan. The island produces an overwhelming share of the world’s most advanced chips — a monopoly-like dependency with enormous geopolitical risk potential.

China is pursuing the strategic goal of building its own semiconductor ecosystem. Massive state subsidies are driving this process forward. Chinese companies are indeed making increasing progress, especially with specialized chips, but in high-performance computing, the gap with the leading western providers remains significant.

More decisive than the technological race is the structural dependency on Taiwan. A large share of the world’s most advanced chips is manufactured there.

The situation is often compared to Europe's past dependency on Russian energy — but this comparison falls short. While energy could be sourced from other suppliers in the medium term, there are no short-term alternatives for cutting-edge semiconductors currently. This technological vulnerability runs deeper and is more challenging to resolve over time. The growing geopolitical tensions between China and Taiwan — from military maneuvers to economic countermeasures — significantly exacerbate the risk for 2026. A conflict or blockade would have immediate consequences:

Collapse of global supply chains

Halt in industrial production

Exploding inflation and plummeting corporate profits

For investors, this means: Geographic diversification and the resilience of supply chains will become the decisive evaluation criteria in 2026.

Conclusion for 2026: A complex environment requires active management

2026 remains characterized by the dominance of Artificial Intelligence — however, with a more differentiated view on the associated risks. Energy supply, financing, and geopolitics come increasingly into focus and increasingly determine the sustainability of growth.

For investors, this does not mean turning away from the AI trend but keeping it consciously and actively managed.

This is exactly where UnitPlus comes in. With actively managed ETF portfolios in collaboration with renowned partners like J.P. Morgan Asset Management and Goldman Sachs Asset Management, investors gain access to professional strategies tailored to a complex market environment like 2026.

Whether with a pure equity portfolio like AktienPlus or a balanced solution like MultiPlus: UnitPlus combines active management, transparency, and daily availability — so that opportunities can be seized and risks can be controlled.

Oussama Aissani

" width="18.358555075662473px"><path d="M 15.333 6.557 C 15.345 5.692 15.574 4.844 16.001 4.092 C 16.428 3.339 17.039 2.707 17.775 2.254 C 17.307 1.586 16.69 1.036 15.972 0.648 C 15.254 0.259 14.455 0.044 13.64 0.019 C 11.9 -0.164 10.213 1.06 9.326 1.06 C 8.422 1.06 7.057 0.037 5.587 0.067 C 4.636 0.098 3.709 0.374 2.897 0.87 C 2.084 1.365 1.414 2.062 0.952 2.894 C -1.052 6.363 0.442 11.463 2.362 14.267 C 3.323 15.641 4.445 17.175 5.914 17.12 C 7.351 17.061 7.888 16.204 9.623 16.204 C 11.342 16.204 11.846 17.12 13.344 17.086 C 14.887 17.061 15.858 15.706 16.785 14.32 C 17.475 13.341 18.006 12.26 18.359 11.115 C 17.462 10.736 16.698 10.102 16.16 9.291 C 15.622 8.481 15.335 7.53 15.333 6.557 Z" fill="rgb(255, 255, 255)" height="17.121899485357133px" id="WpGc1Eutl" transform="translate(0 5.443)" width="18.358555075662473px"/><path d="M 3.364 3.617 C 4.205 2.608 4.619 1.31 4.519 0 C 3.234 0.135 2.048 0.749 1.195 1.72 C 0.779 2.194 0.459 2.746 0.256 3.343 C 0.053 3.941 -0.031 4.573 0.01 5.203 C 0.653 5.21 1.288 5.07 1.869 4.796 C 2.45 4.521 2.961 4.118 3.364 3.617 Z" fill="rgb(255, 255, 255)" height="5.20319404213897px" id="ZowOfaNwx" transform="translate(9.139 0)" width="4.53379423829281px"/></g><g d="M 8.16 9.605 L 3.255 9.605 L 2.078 13.083 L 0 13.083 L 4.646 0.215 L 6.804 0.215 L 11.45 13.083 L 9.337 13.083 Z M 3.763 8 L 7.651 8 L 5.735 2.355 L 5.681 2.355 Z M 21.484 8.392 C 21.484 11.308 19.923 13.181 17.569 13.181 C 16.972 13.212 16.379 13.075 15.857 12.784 C 15.335 12.494 14.905 12.063 14.617 11.54 L 14.572 11.54 L 14.572 16.186 L 12.646 16.186 L 12.646 3.701 L 14.511 3.701 L 14.511 5.261 L 14.546 5.261 C 14.847 4.741 15.284 4.312 15.81 4.02 C 16.337 3.728 16.932 3.584 17.533 3.603 C 19.914 3.603 21.484 5.485 21.484 8.392 Z M 19.504 8.392 C 19.504 6.493 18.523 5.244 17.025 5.244 C 15.554 5.244 14.564 6.519 14.564 8.392 C 14.564 10.283 15.554 11.549 17.025 11.549 C 18.523 11.549 19.504 10.309 19.504 8.392 Z M 31.81 8.392 C 31.81 11.308 30.25 13.181 27.895 13.181 C 27.298 13.212 26.705 13.075 26.183 12.784 C 25.661 12.494 25.231 12.063 24.943 11.54 L 24.898 11.54 L 24.898 16.186 L 22.973 16.186 L 22.973 3.701 L 24.837 3.701 L 24.837 5.261 L 24.872 5.261 C 25.174 4.741 25.611 4.312 26.137 4.02 C 26.663 3.727 27.258 3.584 27.859 3.603 C 30.24 3.603 31.81 5.485 31.81 8.392 Z M 29.831 8.392 C 29.831 6.493 28.849 5.244 27.351 5.244 C 25.88 5.244 24.89 6.519 24.89 8.392 C 24.89 10.283 25.88 11.549 27.351 11.549 C 28.849 11.549 29.831 10.309 29.831 8.392 Z M 38.633 9.497 C 38.776 10.773 40.016 11.611 41.71 11.611 C 43.333 11.611 44.501 10.773 44.501 9.623 C 44.501 8.624 43.796 8.026 42.129 7.616 L 40.461 7.214 C 38.098 6.643 37.001 5.538 37.001 3.745 C 37.001 1.525 38.936 0 41.683 0 C 44.403 0 46.267 1.525 46.329 3.745 L 44.385 3.745 C 44.269 2.461 43.207 1.686 41.656 1.686 C 40.105 1.686 39.043 2.47 39.043 3.612 C 39.043 4.521 39.721 5.057 41.38 5.467 L 42.798 5.815 C 45.438 6.439 46.535 7.5 46.535 9.382 C 46.535 11.789 44.617 13.297 41.567 13.297 C 38.713 13.297 36.787 11.825 36.662 9.497 Z M 50.692 1.481 L 50.692 3.701 L 52.476 3.701 L 52.476 5.226 L 50.692 5.226 L 50.692 10.398 C 50.692 11.201 51.049 11.576 51.833 11.576 C 52.045 11.572 52.256 11.557 52.466 11.531 L 52.466 13.047 C 52.114 13.113 51.755 13.143 51.397 13.136 C 49.497 13.136 48.757 12.423 48.757 10.603 L 48.757 5.226 L 47.393 5.226 L 47.393 3.701 L 48.757 3.701 L 48.757 1.481 Z M 53.508 8.392 C 53.508 5.44 55.246 3.585 57.957 3.585 C 60.677 3.585 62.408 5.44 62.408 8.392 C 62.408 11.352 60.687 13.199 57.957 13.199 C 55.229 13.199 53.508 11.352 53.508 8.392 Z M 60.446 8.392 C 60.446 6.367 59.518 5.172 57.957 5.172 C 56.397 5.172 55.47 6.376 55.47 8.392 C 55.47 10.425 56.397 11.611 57.957 11.611 C 59.518 11.611 60.446 10.425 60.446 8.392 Z M 63.996 3.701 L 65.833 3.701 L 65.833 5.298 L 65.878 5.298 C 66.002 4.799 66.294 4.358 66.705 4.05 C 67.116 3.741 67.621 3.583 68.134 3.603 C 68.356 3.602 68.578 3.626 68.794 3.675 L 68.794 5.476 C 68.514 5.39 68.222 5.351 67.929 5.36 C 67.649 5.348 67.37 5.398 67.111 5.504 C 66.853 5.611 66.62 5.772 66.429 5.977 C 66.238 6.182 66.094 6.426 66.007 6.692 C 65.919 6.958 65.891 7.24 65.922 7.518 L 65.922 13.083 L 63.996 13.083 Z M 77.672 10.327 C 77.413 12.03 75.755 13.199 73.633 13.199 C 70.903 13.199 69.209 11.37 69.209 8.437 C 69.209 5.494 70.913 3.585 73.552 3.585 C 76.147 3.585 77.78 5.368 77.78 8.213 L 77.78 8.873 L 71.153 8.873 L 71.153 8.989 C 71.123 9.335 71.166 9.682 71.28 10.01 C 71.394 10.337 71.577 10.636 71.816 10.887 C 72.054 11.139 72.344 11.337 72.665 11.467 C 72.986 11.598 73.331 11.659 73.677 11.647 C 74.132 11.689 74.589 11.584 74.979 11.346 C 75.37 11.108 75.673 10.751 75.844 10.327 Z M 71.162 7.527 L 75.853 7.527 C 75.87 7.217 75.823 6.906 75.715 6.614 C 75.606 6.323 75.439 6.057 75.223 5.834 C 75.006 5.61 74.747 5.434 74.459 5.315 C 74.171 5.197 73.863 5.139 73.552 5.146 C 73.238 5.144 72.927 5.204 72.637 5.323 C 72.347 5.442 72.083 5.617 71.861 5.839 C 71.639 6.06 71.463 6.323 71.343 6.613 C 71.223 6.903 71.162 7.213 71.162 7.527 Z" fill="transparent" height="16.186400346759847px" id="SxCFNVsxl" transform="translate(35.564 11.077)" width="77.77950372314453px"><path d="M 8.16 9.39 L 3.255 9.39 L 2.078 12.868 L 0 12.868 L 4.646 0 L 6.804 0 L 11.45 12.868 L 9.337 12.868 Z M 3.763 7.785 L 7.651 7.785 L 5.735 2.14 L 5.681 2.14 Z" fill="rgb(255, 255, 255)" height="12.867899999999999px" id="BeFIH2l7O" transform="translate(0 0.215)" width="11.450099999999999px"/><path d="M 8.837 4.791 C 8.837 7.707 7.277 9.58 4.922 9.58 C 4.326 9.611 3.732 9.474 3.21 9.183 C 2.688 8.893 2.259 8.462 1.97 7.938 L 1.926 7.938 L 1.926 12.585 L 0 12.585 L 0 0.1 L 1.864 0.1 L 1.864 1.66 L 1.899 1.66 C 2.201 1.14 2.638 0.71 3.164 0.418 C 3.69 0.126 4.285 -0.018 4.887 0.002 C 7.268 0.002 8.837 1.884 8.837 4.791 Z M 6.858 4.791 C 6.858 2.892 5.876 1.643 4.379 1.643 C 2.907 1.643 1.918 2.918 1.918 4.791 C 1.918 6.682 2.907 7.948 4.379 7.948 C 5.876 7.948 6.858 6.708 6.858 4.791 Z" fill="rgb(255, 255, 255)" height="12.58523071383529px" id="o_v6WXgcK" transform="translate(12.646 3.601)" width="8.837399999999995px"/><path d="M 8.837 4.791 C 8.837 7.707 7.277 9.58 4.922 9.58 C 4.326 9.611 3.732 9.474 3.21 9.183 C 2.688 8.893 2.259 8.462 1.97 7.938 L 1.926 7.938 L 1.926 12.585 L 0 12.585 L 0 0.1 L 1.864 0.1 L 1.864 1.66 L 1.899 1.66 C 2.201 1.14 2.638 0.71 3.164 0.418 C 3.69 0.126 4.285 -0.018 4.887 0.002 C 7.268 0.002 8.837 1.884 8.837 4.791 Z M 6.858 4.791 C 6.858 2.892 5.876 1.643 4.379 1.643 C 2.907 1.643 1.918 2.918 1.918 4.791 C 1.918 6.682 2.907 7.948 4.379 7.948 C 5.876 7.948 6.858 6.708 6.858 4.791 Z" fill="rgb(255, 255, 255)" height="12.585231714252522px" id="SDStu4mWo" transform="translate(22.973 3.601)" width="8.837399999999995px"/><path d="M 1.971 9.497 C 2.114 10.773 3.354 11.611 5.048 11.611 C 6.671 11.611 7.838 10.773 7.838 9.623 C 7.838 8.624 7.134 8.026 5.466 7.616 L 3.799 7.214 C 1.436 6.643 0.339 5.538 0.339 3.745 C 0.339 1.525 2.274 0 5.021 0 C 7.74 0 9.604 1.525 9.667 3.745 L 7.723 3.745 C 7.607 2.461 6.545 1.686 4.994 1.686 C 3.443 1.686 2.381 2.47 2.381 3.612 C 2.381 4.521 3.059 5.057 4.718 5.467 L 6.135 5.815 C 8.776 6.439 9.873 7.5 9.873 9.382 C 9.873 11.789 7.955 13.297 4.905 13.297 C 2.051 13.297 0.124 11.825 0 9.497 Z" fill="rgb(255, 255, 255)" height="13.296999999999997px" id="eWV_R1YMk" transform="translate(36.662 0)" width="9.872500000000002px"/><path d="M 3.299 0 L 3.299 2.22 L 5.083 2.22 L 5.083 3.745 L 3.299 3.745 L 3.299 8.917 C 3.299 9.721 3.656 10.095 4.44 10.095 C 4.652 10.091 4.864 10.077 5.074 10.051 L 5.074 11.566 C 4.721 11.632 4.363 11.662 4.004 11.656 C 2.105 11.656 1.364 10.942 1.364 9.123 L 1.364 3.745 L 0 3.745 L 0 2.22 L 1.364 2.22 L 1.364 0 Z" fill="rgb(255, 255, 255)" height="11.65652033765733px" id="ODxsQPJca" transform="translate(47.393 1.481)" width="5.083000000000013px"/><path d="M 0 4.807 C 0 1.855 1.739 0 4.45 0 C 7.17 0 8.9 1.855 8.9 4.807 C 8.9 7.767 7.179 9.613 4.45 9.613 C 1.721 9.613 0 7.767 0 4.807 Z M 6.938 4.807 C 6.938 2.782 6.01 1.587 4.45 1.587 C 2.889 1.587 1.962 2.791 1.962 4.807 C 1.962 6.84 2.889 8.026 4.45 8.026 C 6.01 8.026 6.938 6.84 6.938 4.807 Z" fill="rgb(255, 255, 255)" height="9.613499999999998px" id="ViJ3M0PCh" transform="translate(53.508 3.585)" width="8.900000000000006px"/><path d="M 0 0.1 L 1.837 0.1 L 1.837 1.697 L 1.881 1.697 C 2.005 1.198 2.297 0.757 2.709 0.448 C 3.12 0.14 3.624 -0.018 4.137 0.002 C 4.359 0.001 4.581 0.025 4.797 0.073 L 4.797 1.875 C 4.517 1.789 4.225 1.75 3.932 1.758 C 3.652 1.747 3.373 1.796 3.114 1.903 C 2.856 2.01 2.623 2.171 2.432 2.376 C 2.242 2.581 2.097 2.825 2.01 3.091 C 1.922 3.357 1.894 3.639 1.925 3.917 L 1.925 9.482 L 0 9.482 Z" fill="rgb(255, 255, 255)" height="9.481544391133383px" id="hGe7905AD" transform="translate(63.996 3.601)" width="4.797499999999999px"/><path d="M 8.463 6.742 C 8.204 8.445 6.546 9.613 4.424 9.613 C 1.694 9.613 0 7.785 0 4.851 C 0 1.909 1.704 0 4.343 0 C 6.938 0 8.571 1.783 8.571 4.628 L 8.571 5.287 L 1.944 5.287 L 1.944 5.404 C 1.914 5.749 1.957 6.097 2.071 6.424 C 2.185 6.752 2.368 7.051 2.607 7.302 C 2.845 7.553 3.135 7.751 3.456 7.882 C 3.777 8.013 4.122 8.074 4.468 8.061 C 4.923 8.104 5.38 7.998 5.77 7.761 C 6.161 7.523 6.464 7.165 6.635 6.742 Z M 1.953 3.942 L 6.644 3.942 C 6.661 3.631 6.614 3.32 6.506 3.029 C 6.397 2.738 6.23 2.472 6.014 2.248 C 5.797 2.025 5.538 1.848 5.25 1.73 C 4.962 1.611 4.654 1.554 4.343 1.56 C 4.029 1.559 3.718 1.619 3.428 1.738 C 3.138 1.857 2.874 2.032 2.652 2.253 C 2.43 2.475 2.254 2.738 2.134 3.028 C 2.014 3.317 1.953 3.628 1.953 3.942 Z" fill="rgb(255, 255, 255)" height="9.613499999999998px" id="jBEmOj0K3" transform="translate(69.209 3.585)" width="8.570999999999998px"/></g></svg>)

"/><stop offset="1" stop-color="rgb(0, 227, 255)"/></linearGradient><linearGradient id="S0EJ4cUC8-1410590420-linear-gradient" x1="1" x2="0" y1="0.4974874371859296" y2="0.5025125628140704"><stop offset="0" stop-color="rgb(255, 224, 0)"/><stop offset="1" stop-color="rgb(255, 156, 0)"/></linearGradient><linearGradient id="W7knJB4_M-1410590420-linear-gradient" x1="0.7912938134313463" x2="0.20870618656865375" y1="0" y2="1"><stop offset="0" stop-color="rgb(255, 58, 68)"/><stop offset="1" stop-color="rgb(195, 17, 98)"/></linearGradient><linearGradient id="zgr49xREg-1410590420-linear-gradient" x1="0.20324242178162366" x2="0.7967575782183763" y1="0" y2="1"><stop offset="0" stop-color="rgb(50, 160, 113)"/><stop offset="1" stop-color="rgb(0, 240, 118)"/></linearGradient></defs><path d="M 28.663 8.179 C 28.663 10.415 26.916 12.056 24.76 12.056 C 22.616 12.056 20.857 10.406 20.857 8.179 C 20.857 5.932 22.604 4.303 24.76 4.303 C 26.916 4.303 28.663 5.932 28.663 8.179 Z M 26.954 8.17 C 26.954 6.773 25.939 5.821 24.76 5.821 C 23.583 5.821 22.565 6.773 22.565 8.17 C 22.565 9.547 23.58 10.52 24.76 10.52 C 25.939 10.52 26.957 9.556 26.954 8.17 Z M 20.147 8.179 C 20.147 10.415 18.4 12.056 16.244 12.056 C 14.1 12.056 12.341 10.406 12.341 8.179 C 12.341 5.932 14.088 4.303 16.244 4.303 C 18.398 4.303 20.147 5.932 20.147 8.179 Z M 18.439 8.17 C 18.439 6.773 17.424 5.821 16.244 5.821 C 15.067 5.821 14.05 6.773 14.05 8.17 C 14.05 9.547 15.065 10.52 16.244 10.52 C 17.424 10.52 18.439 9.556 18.439 8.17 Z M 6.11 5.469 L 11.689 5.469 C 11.75 5.762 11.78 6.107 11.78 6.491 C 11.78 7.725 11.435 9.254 10.347 10.338 C 9.28 11.442 7.929 12.028 6.13 12.028 C 2.794 12.028 0 9.334 0 6.014 C 0 2.704 2.797 0 6.13 0 C 7.968 0 9.28 0.72 10.265 1.661 L 9.097 2.824 C 8.388 2.165 7.432 1.649 6.12 1.649 C 3.691 1.649 1.791 3.604 1.791 6.023 C 1.791 8.443 3.691 10.397 6.12 10.397 C 7.697 10.397 8.591 9.77 9.17 9.193 C 9.638 8.727 9.944 8.048 10.064 7.127 L 6.111 7.127 L 6.111 5.487 C 6.111 5.487 6.111 5.471 6.11 5.469 Z M 6.109 5.469 C 6.109 5.469 6.109 5.469 6.11 5.469 Z M 47.74 7.196 L 42.537 9.343 C 42.943 10.122 43.554 10.517 44.428 10.517 C 45.293 10.517 45.902 10.093 46.34 9.445 L 47.661 10.327 C 47.234 10.963 46.198 12.047 44.419 12.047 C 42.204 12.047 40.557 10.347 40.557 8.17 C 40.557 5.864 42.222 4.294 44.225 4.294 C 46.246 4.294 47.232 5.894 47.558 6.764 C 47.558 6.764 47.739 7.194 47.74 7.196 Z M 47.74 7.196 C 47.74 7.196 47.74 7.196 47.74 7.196 Z M 45.728 6.621 C 45.535 6.135 44.966 5.801 44.284 5.801 C 43.42 5.801 42.211 6.562 42.252 8.059 Z M 38.025 0.427 L 39.733 0.427 L 39.733 11.815 L 38.025 11.815 Z M 35.228 5.164 L 35.228 4.526 L 36.843 4.526 L 36.843 11.481 C 36.843 14.346 35.146 15.521 33.143 15.521 C 31.263 15.521 30.125 14.255 29.699 13.233 L 31.184 12.615 C 31.448 13.242 32.098 13.991 33.145 13.991 C 34.425 13.991 35.219 13.194 35.219 11.715 L 35.219 11.158 L 35.157 11.158 C 34.772 11.624 34.028 12.04 33.104 12.04 C 31.154 12.04 29.375 10.358 29.375 8.182 C 29.375 5.996 31.163 4.294 33.104 4.294 C 34.04 4.294 34.772 4.708 35.157 5.164 L 35.219 5.164 C 35.219 5.164 35.23 5.164 35.228 5.164 Z M 35.331 8.182 C 35.331 6.825 34.425 5.823 33.257 5.823 C 32.078 5.823 31.092 6.814 31.092 8.182 C 31.092 9.538 32.078 10.52 33.257 10.52 C 34.427 10.52 35.342 9.538 35.331 8.182 Z M 59.311 3.969 C 59.311 6.137 57.451 7.502 55.56 7.502 L 53.181 7.502 L 53.181 11.815 L 51.472 11.815 L 51.472 0.427 L 55.558 0.427 C 57.458 0.427 59.311 1.802 59.311 3.969 Z M 57.611 3.958 C 57.611 3.056 56.888 2.004 55.608 2.004 L 53.179 2.004 L 53.179 5.912 L 55.608 5.912 C 56.879 5.912 57.611 4.851 57.611 3.958 Z M 69.623 7.439 L 69.623 11.801 L 67.976 11.801 L 67.976 10.92 L 67.915 10.92 C 67.52 11.517 66.888 12.033 65.741 12.033 C 64.246 12.033 62.905 11.051 62.905 9.522 C 62.905 7.852 64.564 6.962 66.199 6.962 C 67.002 6.962 67.673 7.225 67.978 7.398 L 67.978 7.277 C 67.958 6.337 67.064 5.81 66.179 5.81 C 65.547 5.81 64.949 6.023 64.623 6.65 L 63.108 6.023 C 63.637 4.83 64.917 4.283 66.158 4.283 C 68.108 4.283 69.623 5.408 69.623 7.439 Z M 67.968 8.716 C 67.521 8.493 67.165 8.332 66.412 8.332 C 65.58 8.332 64.603 8.666 64.603 9.547 C 64.603 10.247 65.386 10.52 65.945 10.52 C 66.978 10.511 67.845 9.738 67.968 8.716 Z M 77.522 4.526 L 72.829 15.269 L 71.05 15.269 L 72.788 11.431 L 69.738 4.526 L 71.577 4.526 L 73.609 9.466 L 73.671 9.466 L 75.633 4.526 Z M 60.253 0.427 L 61.961 0.427 L 61.961 11.815 L 60.253 11.815 Z" fill="rgb(255, 255, 255)" height="15.520699943542478px" id="zdXxqMe7L" transform="translate(37.565 11.91)" width="77.5215030517578px"/><path d="M 0.417 0.061 C 0.153 0.345 0 0.779 0 1.347 L 0 21.494 C 0 22.062 0.153 22.496 0.427 22.769 L 0.497 22.83 L 11.83 11.542 L 11.83 11.29 L 0.488 0 Z" fill="url(%23h_hJ8vhPB-1410590420-linear-gradient)" height="22.83005px" id="h_hJ8vhPB" transform="translate(9.127 8.194)" width="11.83015px"/><path d="M 3.78 7.793 L 0 4.028 L 0 3.765 L 3.78 0 L 3.862 0.05 L 8.333 2.581 C 9.613 3.299 9.613 4.485 8.333 5.212 L 3.862 7.743 Z" fill="url(%23S0EJ4cUC8-1410590420-linear-gradient)" height="7.793300000000002px" id="S0EJ4cUC8" transform="translate(20.947 15.717)" width="9.292874999999995px"/><path d="M 15.266 3.847 L 11.404 0 L 0 11.358 C 0.417 11.803 1.118 11.854 1.9 11.42 Z" fill="url(%23W7knJB4_M-1410590420-linear-gradient)" height="11.719905464549623px" id="W7knJB4_M" transform="translate(9.545 19.613)" width="15.265580000000002px"/><path d="M 15.266 7.866 L 1.9 0.305 C 1.118 -0.14 0.415 -0.079 0 0.366 L 11.404 11.713 Z" fill="url(%23zgr49xREg-1410590420-linear-gradient)" height="11.71311070273281px" id="zgr49xREg" transform="translate(9.545 7.9)" width="15.265580000000002px"/></svg>)