Rising Interest Rates on the Horizon: Why Professional Cash Management Matters More Than Ever

Geopolitical tensions in the Middle East and the effective closure of the Strait of Hormuz have driven up energy prices worldwide, increasing inflationary pressure. While market participants largely expected stable interest rates at the beginning of the year, investors are now pricing in rate hikes across Europe, the United States, and the United Kingdom.

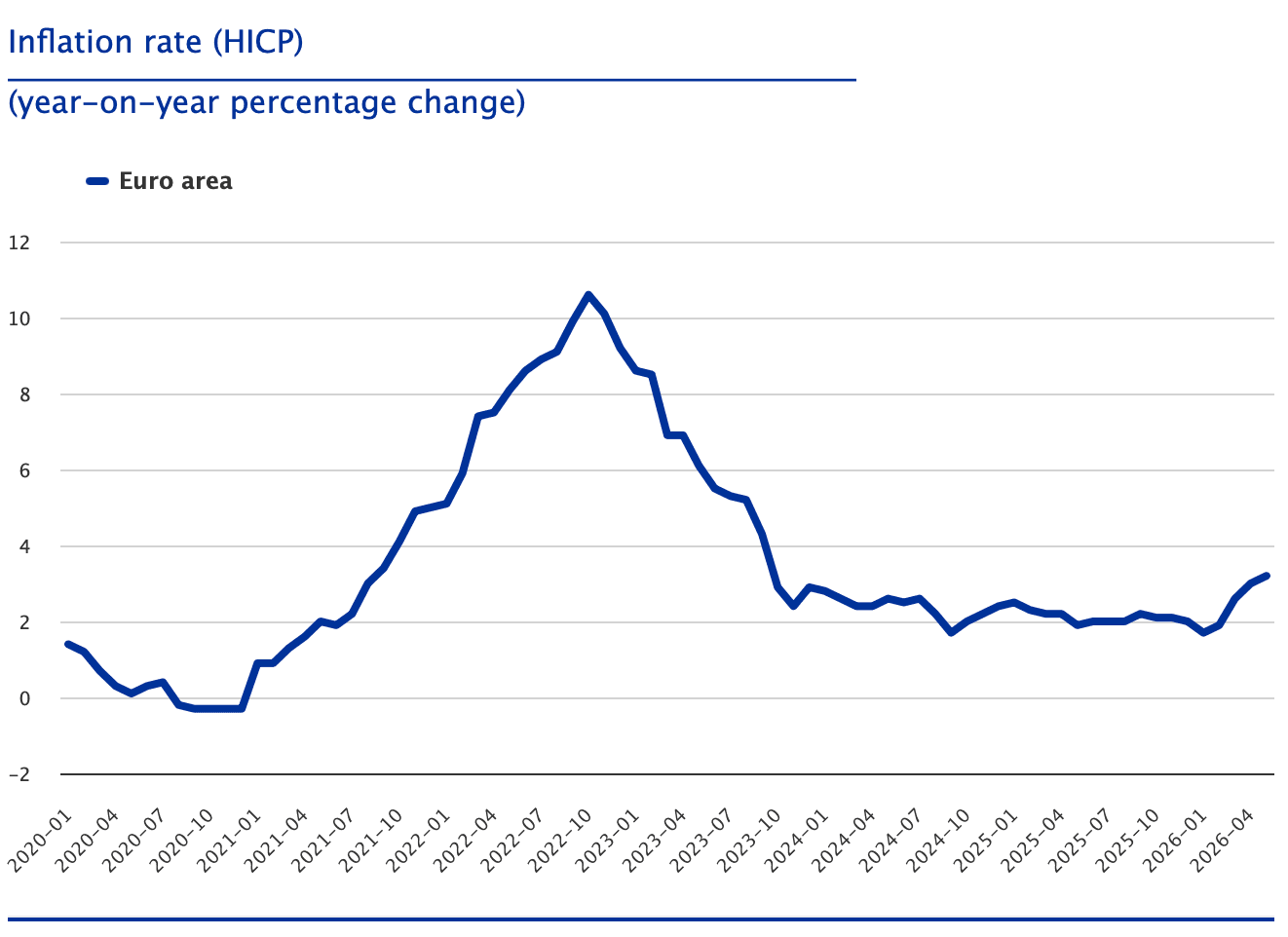

A look at the latest inflation data in the Eurozone highlights the situation: At 3.2%, inflation in May 2026 was significantly above the European Central Bank’s (ECB) target rate of 2%. For businesses, this translates into increasing cost pressure. Rising input costs can erode profit margins, while idle cash held in bank accounts steadily loses purchasing power.

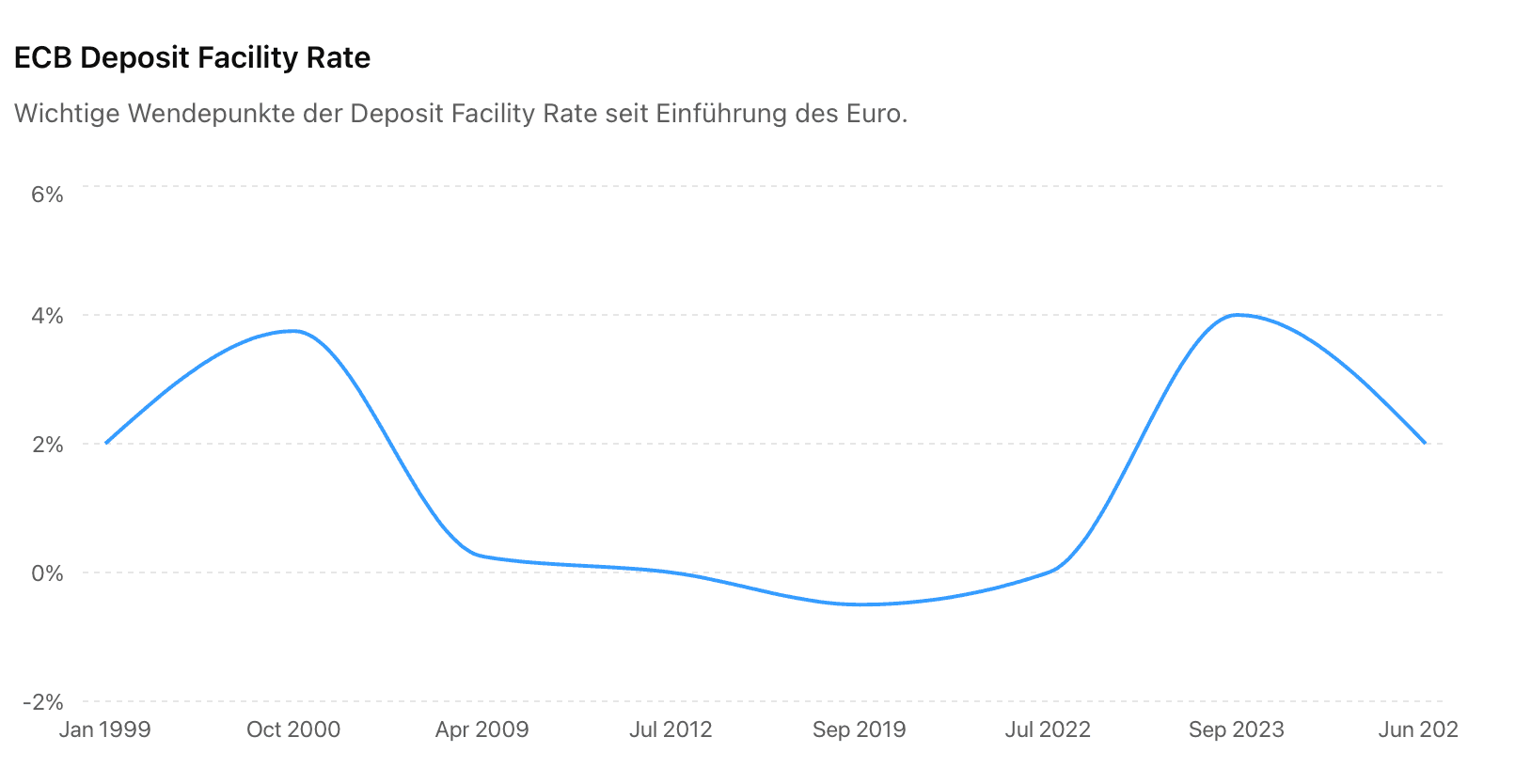

The development of interest rates since the introduction of the euro also illustrates how strongly the monetary policy environment has been shaped by extraordinary events in recent years. The COVID-19 pandemic, the war in Ukraine, and more recent geopolitical conflicts have all contributed to significant fluctuations in interest rates. Against this backdrop, many market participants expect the ECB to raise its key interest rate from 2.00% to 2.25% on June 11. In addition, another 25-basis-point increase later this year is currently anticipated, which would bring the policy rate to 2.50%.

As companies face the combined challenges of rising costs and weaker economic growth, effective liquidity management is becoming increasingly important. What was once viewed primarily as an administrative function is now emerging as a meaningful driver of financial performance.

At the same time, interest rates offered on traditional savings and fixed-term deposit accounts often remain unattractive. Modern cash management solutions enable businesses to deploy their liquidity more efficiently while maintaining the flexibility to respond to changing market conditions.

With UnitPlus Business, we have developed a solution that automatically manages corporate liquidity and invests it in line with prevailing market rates. Funds remain fully accessible at all times and can be withdrawn whenever needed. In addition, assets are held as segregated assets (“special assets”), providing protection beyond statutory deposit insurance and shielding them from potential bank insolvencies.

Implementation is designed to be simple and efficient: onboarding and ongoing administration require only minimal effort. In an environment of rising interest rates, professional cash management can therefore make a meaningful contribution to a company’s financial performance.

Fabian Mohr

" width="18.358555075662473px"><path d="M 15.333 6.557 C 15.345 5.692 15.574 4.844 16.001 4.092 C 16.428 3.339 17.039 2.707 17.775 2.254 C 17.307 1.586 16.69 1.036 15.972 0.648 C 15.254 0.259 14.455 0.044 13.64 0.019 C 11.9 -0.164 10.213 1.06 9.326 1.06 C 8.422 1.06 7.057 0.037 5.587 0.067 C 4.636 0.098 3.709 0.374 2.897 0.87 C 2.084 1.365 1.414 2.062 0.952 2.894 C -1.052 6.363 0.442 11.463 2.362 14.267 C 3.323 15.641 4.445 17.175 5.914 17.12 C 7.351 17.061 7.888 16.204 9.623 16.204 C 11.342 16.204 11.846 17.12 13.344 17.086 C 14.887 17.061 15.858 15.706 16.785 14.32 C 17.475 13.341 18.006 12.26 18.359 11.115 C 17.462 10.736 16.698 10.102 16.16 9.291 C 15.622 8.481 15.335 7.53 15.333 6.557 Z" fill="rgb(255, 255, 255)" height="17.121899485357133px" id="WpGc1Eutl" transform="translate(0 5.443)" width="18.358555075662473px"/><path d="M 3.364 3.617 C 4.205 2.608 4.619 1.31 4.519 0 C 3.234 0.135 2.048 0.749 1.195 1.72 C 0.779 2.194 0.459 2.746 0.256 3.343 C 0.053 3.941 -0.031 4.573 0.01 5.203 C 0.653 5.21 1.288 5.07 1.869 4.796 C 2.45 4.521 2.961 4.118 3.364 3.617 Z" fill="rgb(255, 255, 255)" height="5.20319404213897px" id="ZowOfaNwx" transform="translate(9.139 0)" width="4.53379423829281px"/></g><g d="M 8.16 9.605 L 3.255 9.605 L 2.078 13.083 L 0 13.083 L 4.646 0.215 L 6.804 0.215 L 11.45 13.083 L 9.337 13.083 Z M 3.763 8 L 7.651 8 L 5.735 2.355 L 5.681 2.355 Z M 21.484 8.392 C 21.484 11.308 19.923 13.181 17.569 13.181 C 16.972 13.212 16.379 13.075 15.857 12.784 C 15.335 12.494 14.905 12.063 14.617 11.54 L 14.572 11.54 L 14.572 16.186 L 12.646 16.186 L 12.646 3.701 L 14.511 3.701 L 14.511 5.261 L 14.546 5.261 C 14.847 4.741 15.284 4.312 15.81 4.02 C 16.337 3.728 16.932 3.584 17.533 3.603 C 19.914 3.603 21.484 5.485 21.484 8.392 Z M 19.504 8.392 C 19.504 6.493 18.523 5.244 17.025 5.244 C 15.554 5.244 14.564 6.519 14.564 8.392 C 14.564 10.283 15.554 11.549 17.025 11.549 C 18.523 11.549 19.504 10.309 19.504 8.392 Z M 31.81 8.392 C 31.81 11.308 30.25 13.181 27.895 13.181 C 27.298 13.212 26.705 13.075 26.183 12.784 C 25.661 12.494 25.231 12.063 24.943 11.54 L 24.898 11.54 L 24.898 16.186 L 22.973 16.186 L 22.973 3.701 L 24.837 3.701 L 24.837 5.261 L 24.872 5.261 C 25.174 4.741 25.611 4.312 26.137 4.02 C 26.663 3.727 27.258 3.584 27.859 3.603 C 30.24 3.603 31.81 5.485 31.81 8.392 Z M 29.831 8.392 C 29.831 6.493 28.849 5.244 27.351 5.244 C 25.88 5.244 24.89 6.519 24.89 8.392 C 24.89 10.283 25.88 11.549 27.351 11.549 C 28.849 11.549 29.831 10.309 29.831 8.392 Z M 38.633 9.497 C 38.776 10.773 40.016 11.611 41.71 11.611 C 43.333 11.611 44.501 10.773 44.501 9.623 C 44.501 8.624 43.796 8.026 42.129 7.616 L 40.461 7.214 C 38.098 6.643 37.001 5.538 37.001 3.745 C 37.001 1.525 38.936 0 41.683 0 C 44.403 0 46.267 1.525 46.329 3.745 L 44.385 3.745 C 44.269 2.461 43.207 1.686 41.656 1.686 C 40.105 1.686 39.043 2.47 39.043 3.612 C 39.043 4.521 39.721 5.057 41.38 5.467 L 42.798 5.815 C 45.438 6.439 46.535 7.5 46.535 9.382 C 46.535 11.789 44.617 13.297 41.567 13.297 C 38.713 13.297 36.787 11.825 36.662 9.497 Z M 50.692 1.481 L 50.692 3.701 L 52.476 3.701 L 52.476 5.226 L 50.692 5.226 L 50.692 10.398 C 50.692 11.201 51.049 11.576 51.833 11.576 C 52.045 11.572 52.256 11.557 52.466 11.531 L 52.466 13.047 C 52.114 13.113 51.755 13.143 51.397 13.136 C 49.497 13.136 48.757 12.423 48.757 10.603 L 48.757 5.226 L 47.393 5.226 L 47.393 3.701 L 48.757 3.701 L 48.757 1.481 Z M 53.508 8.392 C 53.508 5.44 55.246 3.585 57.957 3.585 C 60.677 3.585 62.408 5.44 62.408 8.392 C 62.408 11.352 60.687 13.199 57.957 13.199 C 55.229 13.199 53.508 11.352 53.508 8.392 Z M 60.446 8.392 C 60.446 6.367 59.518 5.172 57.957 5.172 C 56.397 5.172 55.47 6.376 55.47 8.392 C 55.47 10.425 56.397 11.611 57.957 11.611 C 59.518 11.611 60.446 10.425 60.446 8.392 Z M 63.996 3.701 L 65.833 3.701 L 65.833 5.298 L 65.878 5.298 C 66.002 4.799 66.294 4.358 66.705 4.05 C 67.116 3.741 67.621 3.583 68.134 3.603 C 68.356 3.602 68.578 3.626 68.794 3.675 L 68.794 5.476 C 68.514 5.39 68.222 5.351 67.929 5.36 C 67.649 5.348 67.37 5.398 67.111 5.504 C 66.853 5.611 66.62 5.772 66.429 5.977 C 66.238 6.182 66.094 6.426 66.007 6.692 C 65.919 6.958 65.891 7.24 65.922 7.518 L 65.922 13.083 L 63.996 13.083 Z M 77.672 10.327 C 77.413 12.03 75.755 13.199 73.633 13.199 C 70.903 13.199 69.209 11.37 69.209 8.437 C 69.209 5.494 70.913 3.585 73.552 3.585 C 76.147 3.585 77.78 5.368 77.78 8.213 L 77.78 8.873 L 71.153 8.873 L 71.153 8.989 C 71.123 9.335 71.166 9.682 71.28 10.01 C 71.394 10.337 71.577 10.636 71.816 10.887 C 72.054 11.139 72.344 11.337 72.665 11.467 C 72.986 11.598 73.331 11.659 73.677 11.647 C 74.132 11.689 74.589 11.584 74.979 11.346 C 75.37 11.108 75.673 10.751 75.844 10.327 Z M 71.162 7.527 L 75.853 7.527 C 75.87 7.217 75.823 6.906 75.715 6.614 C 75.606 6.323 75.439 6.057 75.223 5.834 C 75.006 5.61 74.747 5.434 74.459 5.315 C 74.171 5.197 73.863 5.139 73.552 5.146 C 73.238 5.144 72.927 5.204 72.637 5.323 C 72.347 5.442 72.083 5.617 71.861 5.839 C 71.639 6.06 71.463 6.323 71.343 6.613 C 71.223 6.903 71.162 7.213 71.162 7.527 Z" fill="transparent" height="16.186400346759847px" id="SxCFNVsxl" transform="translate(35.564 11.077)" width="77.77950372314453px"><path d="M 8.16 9.39 L 3.255 9.39 L 2.078 12.868 L 0 12.868 L 4.646 0 L 6.804 0 L 11.45 12.868 L 9.337 12.868 Z M 3.763 7.785 L 7.651 7.785 L 5.735 2.14 L 5.681 2.14 Z" fill="rgb(255, 255, 255)" height="12.867899999999999px" id="BeFIH2l7O" transform="translate(0 0.215)" width="11.450099999999999px"/><path d="M 8.837 4.791 C 8.837 7.707 7.277 9.58 4.922 9.58 C 4.326 9.611 3.732 9.474 3.21 9.183 C 2.688 8.893 2.259 8.462 1.97 7.938 L 1.926 7.938 L 1.926 12.585 L 0 12.585 L 0 0.1 L 1.864 0.1 L 1.864 1.66 L 1.899 1.66 C 2.201 1.14 2.638 0.71 3.164 0.418 C 3.69 0.126 4.285 -0.018 4.887 0.002 C 7.268 0.002 8.837 1.884 8.837 4.791 Z M 6.858 4.791 C 6.858 2.892 5.876 1.643 4.379 1.643 C 2.907 1.643 1.918 2.918 1.918 4.791 C 1.918 6.682 2.907 7.948 4.379 7.948 C 5.876 7.948 6.858 6.708 6.858 4.791 Z" fill="rgb(255, 255, 255)" height="12.58523071383529px" id="o_v6WXgcK" transform="translate(12.646 3.601)" width="8.837399999999995px"/><path d="M 8.837 4.791 C 8.837 7.707 7.277 9.58 4.922 9.58 C 4.326 9.611 3.732 9.474 3.21 9.183 C 2.688 8.893 2.259 8.462 1.97 7.938 L 1.926 7.938 L 1.926 12.585 L 0 12.585 L 0 0.1 L 1.864 0.1 L 1.864 1.66 L 1.899 1.66 C 2.201 1.14 2.638 0.71 3.164 0.418 C 3.69 0.126 4.285 -0.018 4.887 0.002 C 7.268 0.002 8.837 1.884 8.837 4.791 Z M 6.858 4.791 C 6.858 2.892 5.876 1.643 4.379 1.643 C 2.907 1.643 1.918 2.918 1.918 4.791 C 1.918 6.682 2.907 7.948 4.379 7.948 C 5.876 7.948 6.858 6.708 6.858 4.791 Z" fill="rgb(255, 255, 255)" height="12.585231714252522px" id="SDStu4mWo" transform="translate(22.973 3.601)" width="8.837399999999995px"/><path d="M 1.971 9.497 C 2.114 10.773 3.354 11.611 5.048 11.611 C 6.671 11.611 7.838 10.773 7.838 9.623 C 7.838 8.624 7.134 8.026 5.466 7.616 L 3.799 7.214 C 1.436 6.643 0.339 5.538 0.339 3.745 C 0.339 1.525 2.274 0 5.021 0 C 7.74 0 9.604 1.525 9.667 3.745 L 7.723 3.745 C 7.607 2.461 6.545 1.686 4.994 1.686 C 3.443 1.686 2.381 2.47 2.381 3.612 C 2.381 4.521 3.059 5.057 4.718 5.467 L 6.135 5.815 C 8.776 6.439 9.873 7.5 9.873 9.382 C 9.873 11.789 7.955 13.297 4.905 13.297 C 2.051 13.297 0.124 11.825 0 9.497 Z" fill="rgb(255, 255, 255)" height="13.296999999999997px" id="eWV_R1YMk" transform="translate(36.662 0)" width="9.872500000000002px"/><path d="M 3.299 0 L 3.299 2.22 L 5.083 2.22 L 5.083 3.745 L 3.299 3.745 L 3.299 8.917 C 3.299 9.721 3.656 10.095 4.44 10.095 C 4.652 10.091 4.864 10.077 5.074 10.051 L 5.074 11.566 C 4.721 11.632 4.363 11.662 4.004 11.656 C 2.105 11.656 1.364 10.942 1.364 9.123 L 1.364 3.745 L 0 3.745 L 0 2.22 L 1.364 2.22 L 1.364 0 Z" fill="rgb(255, 255, 255)" height="11.65652033765733px" id="ODxsQPJca" transform="translate(47.393 1.481)" width="5.083000000000013px"/><path d="M 0 4.807 C 0 1.855 1.739 0 4.45 0 C 7.17 0 8.9 1.855 8.9 4.807 C 8.9 7.767 7.179 9.613 4.45 9.613 C 1.721 9.613 0 7.767 0 4.807 Z M 6.938 4.807 C 6.938 2.782 6.01 1.587 4.45 1.587 C 2.889 1.587 1.962 2.791 1.962 4.807 C 1.962 6.84 2.889 8.026 4.45 8.026 C 6.01 8.026 6.938 6.84 6.938 4.807 Z" fill="rgb(255, 255, 255)" height="9.613499999999998px" id="ViJ3M0PCh" transform="translate(53.508 3.585)" width="8.900000000000006px"/><path d="M 0 0.1 L 1.837 0.1 L 1.837 1.697 L 1.881 1.697 C 2.005 1.198 2.297 0.757 2.709 0.448 C 3.12 0.14 3.624 -0.018 4.137 0.002 C 4.359 0.001 4.581 0.025 4.797 0.073 L 4.797 1.875 C 4.517 1.789 4.225 1.75 3.932 1.758 C 3.652 1.747 3.373 1.796 3.114 1.903 C 2.856 2.01 2.623 2.171 2.432 2.376 C 2.242 2.581 2.097 2.825 2.01 3.091 C 1.922 3.357 1.894 3.639 1.925 3.917 L 1.925 9.482 L 0 9.482 Z" fill="rgb(255, 255, 255)" height="9.481544391133383px" id="hGe7905AD" transform="translate(63.996 3.601)" width="4.797499999999999px"/><path d="M 8.463 6.742 C 8.204 8.445 6.546 9.613 4.424 9.613 C 1.694 9.613 0 7.785 0 4.851 C 0 1.909 1.704 0 4.343 0 C 6.938 0 8.571 1.783 8.571 4.628 L 8.571 5.287 L 1.944 5.287 L 1.944 5.404 C 1.914 5.749 1.957 6.097 2.071 6.424 C 2.185 6.752 2.368 7.051 2.607 7.302 C 2.845 7.553 3.135 7.751 3.456 7.882 C 3.777 8.013 4.122 8.074 4.468 8.061 C 4.923 8.104 5.38 7.998 5.77 7.761 C 6.161 7.523 6.464 7.165 6.635 6.742 Z M 1.953 3.942 L 6.644 3.942 C 6.661 3.631 6.614 3.32 6.506 3.029 C 6.397 2.738 6.23 2.472 6.014 2.248 C 5.797 2.025 5.538 1.848 5.25 1.73 C 4.962 1.611 4.654 1.554 4.343 1.56 C 4.029 1.559 3.718 1.619 3.428 1.738 C 3.138 1.857 2.874 2.032 2.652 2.253 C 2.43 2.475 2.254 2.738 2.134 3.028 C 2.014 3.317 1.953 3.628 1.953 3.942 Z" fill="rgb(255, 255, 255)" height="9.613499999999998px" id="jBEmOj0K3" transform="translate(69.209 3.585)" width="8.570999999999998px"/></g></svg>)

"/><stop offset="1" stop-color="rgb(0, 227, 255)"/></linearGradient><linearGradient id="S0EJ4cUC8-1410590420-linear-gradient" x1="1" x2="0" y1="0.4974874371859296" y2="0.5025125628140704"><stop offset="0" stop-color="rgb(255, 224, 0)"/><stop offset="1" stop-color="rgb(255, 156, 0)"/></linearGradient><linearGradient id="W7knJB4_M-1410590420-linear-gradient" x1="0.7912938134313463" x2="0.20870618656865375" y1="0" y2="1"><stop offset="0" stop-color="rgb(255, 58, 68)"/><stop offset="1" stop-color="rgb(195, 17, 98)"/></linearGradient><linearGradient id="zgr49xREg-1410590420-linear-gradient" x1="0.20324242178162366" x2="0.7967575782183763" y1="0" y2="1"><stop offset="0" stop-color="rgb(50, 160, 113)"/><stop offset="1" stop-color="rgb(0, 240, 118)"/></linearGradient></defs><path d="M 28.663 8.179 C 28.663 10.415 26.916 12.056 24.76 12.056 C 22.616 12.056 20.857 10.406 20.857 8.179 C 20.857 5.932 22.604 4.303 24.76 4.303 C 26.916 4.303 28.663 5.932 28.663 8.179 Z M 26.954 8.17 C 26.954 6.773 25.939 5.821 24.76 5.821 C 23.583 5.821 22.565 6.773 22.565 8.17 C 22.565 9.547 23.58 10.52 24.76 10.52 C 25.939 10.52 26.957 9.556 26.954 8.17 Z M 20.147 8.179 C 20.147 10.415 18.4 12.056 16.244 12.056 C 14.1 12.056 12.341 10.406 12.341 8.179 C 12.341 5.932 14.088 4.303 16.244 4.303 C 18.398 4.303 20.147 5.932 20.147 8.179 Z M 18.439 8.17 C 18.439 6.773 17.424 5.821 16.244 5.821 C 15.067 5.821 14.05 6.773 14.05 8.17 C 14.05 9.547 15.065 10.52 16.244 10.52 C 17.424 10.52 18.439 9.556 18.439 8.17 Z M 6.11 5.469 L 11.689 5.469 C 11.75 5.762 11.78 6.107 11.78 6.491 C 11.78 7.725 11.435 9.254 10.347 10.338 C 9.28 11.442 7.929 12.028 6.13 12.028 C 2.794 12.028 0 9.334 0 6.014 C 0 2.704 2.797 0 6.13 0 C 7.968 0 9.28 0.72 10.265 1.661 L 9.097 2.824 C 8.388 2.165 7.432 1.649 6.12 1.649 C 3.691 1.649 1.791 3.604 1.791 6.023 C 1.791 8.443 3.691 10.397 6.12 10.397 C 7.697 10.397 8.591 9.77 9.17 9.193 C 9.638 8.727 9.944 8.048 10.064 7.127 L 6.111 7.127 L 6.111 5.487 C 6.111 5.487 6.111 5.471 6.11 5.469 Z M 6.109 5.469 C 6.109 5.469 6.109 5.469 6.11 5.469 Z M 47.74 7.196 L 42.537 9.343 C 42.943 10.122 43.554 10.517 44.428 10.517 C 45.293 10.517 45.902 10.093 46.34 9.445 L 47.661 10.327 C 47.234 10.963 46.198 12.047 44.419 12.047 C 42.204 12.047 40.557 10.347 40.557 8.17 C 40.557 5.864 42.222 4.294 44.225 4.294 C 46.246 4.294 47.232 5.894 47.558 6.764 C 47.558 6.764 47.739 7.194 47.74 7.196 Z M 47.74 7.196 C 47.74 7.196 47.74 7.196 47.74 7.196 Z M 45.728 6.621 C 45.535 6.135 44.966 5.801 44.284 5.801 C 43.42 5.801 42.211 6.562 42.252 8.059 Z M 38.025 0.427 L 39.733 0.427 L 39.733 11.815 L 38.025 11.815 Z M 35.228 5.164 L 35.228 4.526 L 36.843 4.526 L 36.843 11.481 C 36.843 14.346 35.146 15.521 33.143 15.521 C 31.263 15.521 30.125 14.255 29.699 13.233 L 31.184 12.615 C 31.448 13.242 32.098 13.991 33.145 13.991 C 34.425 13.991 35.219 13.194 35.219 11.715 L 35.219 11.158 L 35.157 11.158 C 34.772 11.624 34.028 12.04 33.104 12.04 C 31.154 12.04 29.375 10.358 29.375 8.182 C 29.375 5.996 31.163 4.294 33.104 4.294 C 34.04 4.294 34.772 4.708 35.157 5.164 L 35.219 5.164 C 35.219 5.164 35.23 5.164 35.228 5.164 Z M 35.331 8.182 C 35.331 6.825 34.425 5.823 33.257 5.823 C 32.078 5.823 31.092 6.814 31.092 8.182 C 31.092 9.538 32.078 10.52 33.257 10.52 C 34.427 10.52 35.342 9.538 35.331 8.182 Z M 59.311 3.969 C 59.311 6.137 57.451 7.502 55.56 7.502 L 53.181 7.502 L 53.181 11.815 L 51.472 11.815 L 51.472 0.427 L 55.558 0.427 C 57.458 0.427 59.311 1.802 59.311 3.969 Z M 57.611 3.958 C 57.611 3.056 56.888 2.004 55.608 2.004 L 53.179 2.004 L 53.179 5.912 L 55.608 5.912 C 56.879 5.912 57.611 4.851 57.611 3.958 Z M 69.623 7.439 L 69.623 11.801 L 67.976 11.801 L 67.976 10.92 L 67.915 10.92 C 67.52 11.517 66.888 12.033 65.741 12.033 C 64.246 12.033 62.905 11.051 62.905 9.522 C 62.905 7.852 64.564 6.962 66.199 6.962 C 67.002 6.962 67.673 7.225 67.978 7.398 L 67.978 7.277 C 67.958 6.337 67.064 5.81 66.179 5.81 C 65.547 5.81 64.949 6.023 64.623 6.65 L 63.108 6.023 C 63.637 4.83 64.917 4.283 66.158 4.283 C 68.108 4.283 69.623 5.408 69.623 7.439 Z M 67.968 8.716 C 67.521 8.493 67.165 8.332 66.412 8.332 C 65.58 8.332 64.603 8.666 64.603 9.547 C 64.603 10.247 65.386 10.52 65.945 10.52 C 66.978 10.511 67.845 9.738 67.968 8.716 Z M 77.522 4.526 L 72.829 15.269 L 71.05 15.269 L 72.788 11.431 L 69.738 4.526 L 71.577 4.526 L 73.609 9.466 L 73.671 9.466 L 75.633 4.526 Z M 60.253 0.427 L 61.961 0.427 L 61.961 11.815 L 60.253 11.815 Z" fill="rgb(255, 255, 255)" height="15.520699943542478px" id="zdXxqMe7L" transform="translate(37.565 11.91)" width="77.5215030517578px"/><path d="M 0.417 0.061 C 0.153 0.345 0 0.779 0 1.347 L 0 21.494 C 0 22.062 0.153 22.496 0.427 22.769 L 0.497 22.83 L 11.83 11.542 L 11.83 11.29 L 0.488 0 Z" fill="url(%23h_hJ8vhPB-1410590420-linear-gradient)" height="22.83005px" id="h_hJ8vhPB" transform="translate(9.127 8.194)" width="11.83015px"/><path d="M 3.78 7.793 L 0 4.028 L 0 3.765 L 3.78 0 L 3.862 0.05 L 8.333 2.581 C 9.613 3.299 9.613 4.485 8.333 5.212 L 3.862 7.743 Z" fill="url(%23S0EJ4cUC8-1410590420-linear-gradient)" height="7.793300000000002px" id="S0EJ4cUC8" transform="translate(20.947 15.717)" width="9.292874999999995px"/><path d="M 15.266 3.847 L 11.404 0 L 0 11.358 C 0.417 11.803 1.118 11.854 1.9 11.42 Z" fill="url(%23W7knJB4_M-1410590420-linear-gradient)" height="11.719905464549623px" id="W7knJB4_M" transform="translate(9.545 19.613)" width="15.265580000000002px"/><path d="M 15.266 7.866 L 1.9 0.305 C 1.118 -0.14 0.415 -0.079 0 0.366 L 11.404 11.713 Z" fill="url(%23zgr49xREg-1410590420-linear-gradient)" height="11.71311070273281px" id="zgr49xREg" transform="translate(9.545 7.9)" width="15.265580000000002px"/></svg>)