On Wednesday, August 14th, we had the privilege of hosting a webinar with Tom Griffiths, a seasoned Portfolio Manager at Goldman Sachs Asset Management (GSAM). For those who couldn’t join us live, this blog post captures the essence of the discussion, highlighting the most important insights and takeaways.

The session began with an introduction to UnitPlus, outlining our mission and the rationale behind our operations. We emphasised our commitment to providing innovative financial solutions that enhance liquidity management for businesses.

Following this, the discussion delved into the complexities of money markets, offering a comprehensive overview of their operations and significance. We explored how money market funds function, and also addressed the potential impacts of major future events on the markets, equipping participants with a forward-looking perspective on financial planning and risk management. This insight is crucial for navigating economic uncertainties and optimising investment strategies.

Table of Contents

CEO Insights: What We Stand For at UnitPlus Business

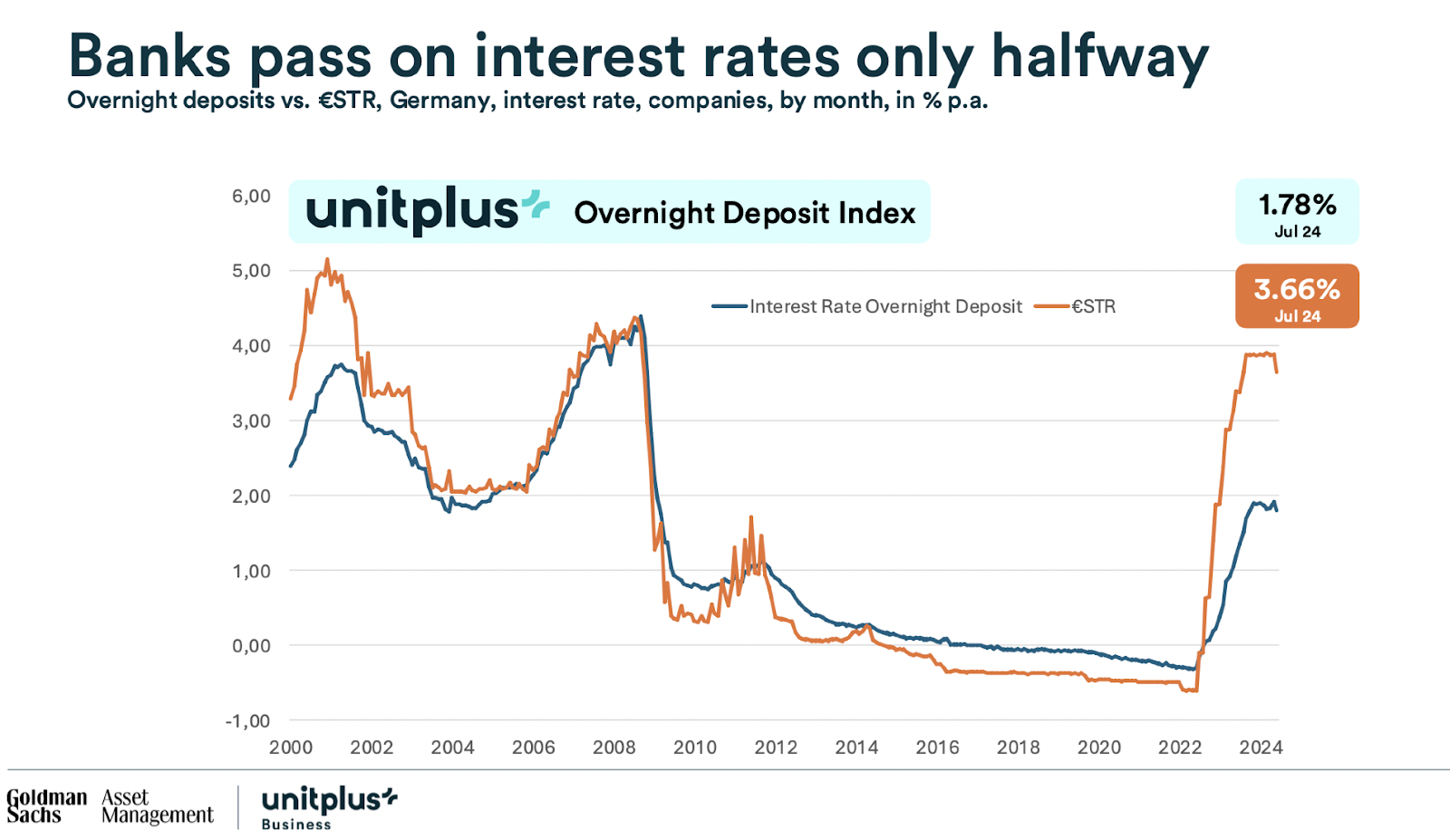

UnitPlus Business’ focus is on addressing the challenges posed by the sluggish pass-through of interest rate rises by banks to their depositors in Germany. Despite the European Central Bank (ECB) raising rates over the previous years, banks often pass on only a fraction of these increases, resulting in deposit rates that remain low (1.78% as of Jul 2024). This contrasts sharply with money market funds (MMFs), which offer returns more aligned with ECB rates, (UnitPlus Business provided a return of 3.66% as of Jul’24).

The graph below clearly demonstrates the gap between the average overnight deposit rate offered to companies (represented by an index developed by UnitPlus with Barkow Consulting – know more here) and the potential returns achievable through investing with UnitPlus Business.

This discrepancy highlights a significant issue for businesses and individuals seeking competitive returns. To solve this problem, UnitPlus Business has developed an innovative product that allows SMEs to invest in MMFs, thereby accessing higher returns. This empowers businesses to optimize their financial strategies, ensuring they can navigate economic uncertainties with enhanced liquidity and profitability.

Brief Background on Money Market

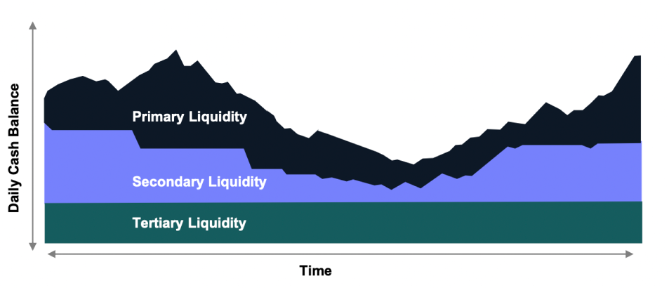

Liquidity can be broadly categorized into three tiers based on the investment horizon:

1. Primary: This category includes Bank Deposits and Money Market Funds (MMFs) with an investment horizon of 0 to 12 months.MMFs, which are regulated mutual funds, invest in high-quality, short-term debt instruments. They offer an opportunity to earn a yield while maintaining access to the underlying assets, making them an attractive option for short-term liquidity needs.

2. Secondary: This category consists of short-duration investments with an investment horizon of 12 months or longer. These investments offer a balance between liquidity and potential returns, suitable for investors with a slightly longer time frame.

3. Tertiary: This category includes broad fixed-income investments with an indefinite investment horizon. These investments are designed for long-term growth and may involve less liquidity, making them suitable for investors with a longer-term perspective.

Objectives of MMFs

1. Preservation of Capital (Stability)

2. Maintain daily liquidity

3. Offer attractive yields

With these objectives in mind, a typical MMF would invest in instruments which have a maturity period of up to one year, with a significant concentration in the one to three-month range. Allocation is typically as below –

o Overnight Deposits: Approximately 40% of the Assets Under Management (AUM) is typically invested in overnight deposits.

o Bank Deposits: While MMFs can invest in bank deposits, they are restricted to a maximum of 5% of AUM in any single bank. This limitation emphasizes the importance of diversifying investments to reduce concentration risk.

o Longer-Term Assets: The remaining 60% of AUM is usually allocated to comparatively longer-term assets. This includes:

· Government bonds from countries

· Loans to corporations

· Investments in high-quality or systemically important banks

Why invest in MMF over Bank Deposits

1. Segregated assets: Deposits in banks are usually unsecured general liabilities. Whereas in MMFs a custodian account is opened for a fund specifically and the assets are held independently from the asset manager. Hence resulting in a lot more protection than parking your cash in one single bank account.

2. Diversification: MMFs invest in many different types of holdings (100+), which is much safer than depositing 100% of your funds in one single bank.

3. Liquidity: MMFs ensure daily liquidity by investing a large proportion of their AUM in liquid securities. They also do not impose any minimum redemption amount restrictions, lock up period or penalties.

– For eg: 40% of the total AUM is usually invested in overnight liquidity (well above the 10% regulatory minimum).

Insights on Future Events

Resilience in the Global Economy

Despite initial predictions of a downturn, the global economy has demonstrated remarkable resilience. Indicators such as robust labor markets and resilient growth, particularly in the Eurozone, have exceeded expectations. However, concerns remain about a potential recession in the Eurozone, despite its current stronger-than-expected growth performance.

Future of interest rates

The future of interest rates is currently shaped by market expectations of cuts at upcoming meetings, influenced by several critical factors:

o Service Inflation Rates: Both the Eurozone and the UK are experiencing service inflation rates that exceed their targets. This disparity could significantly impact monetary policy decisions in these regions.

o Wage Growth in the Eurozone: With wage growth at 4.7% in the Eurozone, policymakers are adopting a cautious stance, remaining alert to potential inflationary pressures.

o Economic Uncertainty in the US: Signs of a weakening labor market in the US raises concerns as well. If the Federal Reserve decides to implement rate cuts, it is likely that the ECB will adjust its policies accordingly as well, responding to shifts in the US economy.

These elements collectively indicate a complex landscape for future interest rates, where central banks must carefully navigate inflation targets and economic conditions.

What can we learn from blue chip companies and what to avoid?

Blue chip companies prioritize capital preservation by avoiding over-reliance on a single institution. The recent crises at Silicon Valley Bank and Credit Suisse highlight the risks of concentrating investments in one bank. These events underscore the importance of diversification in protecting capital.

Investors and small businesses can learn from blue chip practices to better safeguard their assets against financial instability.

By understanding these economic dynamics and investment strategies, stakeholders can better navigate the complexities of the current global financial landscape.

Disclaimer

The information provided here is not intended as investment advice. The views expressed by Tom are solely his own and do not reflect the opinions or positions of GSAM. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.